Why should you care what your business’ break-even point is? What

purpose does it serve to know what it is? More specifically, how do you

determine which of your business costs are fixed and which are

variable? What costs affect your break-even point the most? How often

should this information be calculated? How do you use this information

to better manage your business?

These are some of the questions that need to be answered in order

for you to have a better understanding of the importance of knowing

your break-even point. Let’s first explore the basic question of why

you need to know your break-even point.

Actually, the reason you should care about it is glaringly obvious.

The definition of break-even is "the point at which your revenues

exactly equal your expenses." Or, put in another way, "the company has

neither generated a profit nor sustained a loss."

This is one reason why you should want to know what the break-even

point of your business is. It can tell you how much revenue you need to

generate each day, or each month to pay the bills. It can help you

determine if you should purchase that new piece of equipment. It can

tell you the very first moment at which you even have a chance of

making a profit.

Every shop owner must cover all of the fixed costs, and usually a

certain amount of variable costs, before having the opportunity to make

a profit. Let’s look at an example of a business situation where

knowing your break-even point is helpful.

Say it is the peak sales time of the year. Your sales this month

start out with a bang, just as expected. However, only one week into

what should be the biggest month of the year, sales drop off

drastically. You look for an explanation, any explanation, but none is

found. All that you can tell is that the slow down seems to have

affected everyone in the same business in your marketing area.

This may console you a little, i.e., misery loves company. But it

doesn’t help with the fact that you still have "X" amount of expenses

that you must cover, no matter what the sales volume is.

One purpose of knowing your break-even point is to be able to know

when you have generated enough revenue to cover your expenses. If you

do not generate enough revenue to cover expenses each and every month

of the year, then you need to look at your fixed costs. Your fixed

costs may possibly be too high to support the gross revenue you

generate.

Variable cost importance

In addition to knowing your fixed costs, you should have a good

understanding of your company’s variable costs. You need the

flexibility in your variable costs to sustain profitability during both

the slower sales months as well as during the higher sales months. In

order to achieve this flexibility you must define your fixed and

variable expenses. Fixed costs are rigid or preset, they remain

constant regardless of sales. Variable costs are those costs which you

can drive or affect from day-to-day. They are costs directly associated

with selling your products or services.

Variable costs typically go up as you add more products or services

what you offer. However, you have no real control over fixed costs;

they are what they are. Variable costs you do have some control over;

you can reduce the expenditure for them or eliminate them completely.

There is no perfect classification system for defining fixed and

variable costs. Let’s look at an example, electricity, which makes that

more understandable. What is the "minimum use" electric bill you would

get from the local power company if you didn’t even open your doors

this month? (For our company it would be about $50.) Then compare this

amount to the electrical bill you typically pay in a month. (For me,

this is about $800.) In this example, I might place $50 in fixed

expenses for electricity use, and $750 in the variable expenses for

electricity use.

Another way to classify electricity use would be to place all

utility expenses under fixed costs. You see, you can spend the time

necessary to split out these types of expenses between fixed and

variable costs, or you can lump them all together. But whatever you do,

as long as you consistently apply the definition, either way will work.

You’ll end up with the important information you need to establish your

break-even point.

After using break-even point analysis a few times, you may decide to

look more closely at each type of expense. You may decide to record

each expense more precisely as you get used to calculating it. And this

is one of the objectives of knowing your break-even point, i.e., to

scrutinize each expense you have so as to increase your overall profits.

You can, for example, choose to discontinue the uniform service

expenses you provide each employee, in essence turning this into a

variable expense. However, if you have signed a contract with a uniform

service company for the next 12 months, this expense would become a

fixed cost.

An item that might have some controversy as to how it should be

listed in your calculations is depreciation expenses. Many say that you

should use this line item found on your income statement as a fixed

expense in calculating your break-even point. However, I disagree. I

recommend that you use the actual principle and interest payments in

the calculation as a fixed cost.

Remember, the income statement is a valuable financial tool.

However, it is geared toward the collection of taxes from your company

by the government. You did not spend the allowance for depreciation

that is listed on the income statement. It is a figure that the

government is allowing you to list as an expense.

It is likely that you actually spent more for the plant and

equipment, especially when you add in principle payments. If you use

the figure listed on the income statement for depreciation as a fixed

cost, you will have defeated your purpose of calculating the real

break-even point. You need to know in actual dollars what the amount of

revenue you must generate to break-even is. So let’s use the actual

amount that we are spending for both principle and interest.

The fixed expenses portion of your calculation will have the biggest

impact on the amount of revenue which you must generate each month.

This is the hardest one to control also. The local government can raise

your real estate taxes, virtually at anytime, and you must pay them.

Your choices in the above example would be to protest the tax amount

with the local taxing body, perhaps hiring an attorney to do this for

you. Or another option would be to relocate your business to a lower

taxing area. Neither option is easy, but both must be considered if you

are to lower your fixed costs. One benefit of knowing your break-even

point is to actually put a number, a dollar amount, on what you must

generate per day or per month. This is tremendously beneficial

information.

You then have more of the needed information to monitor your

business and your employees. It can help you to determine if you are

overstaffed or understaffed. It can help with the knowledge of what

minimum amount of revenue you will need to generate if you purchase

that new piece of equipment.

It can also help you justify the decision to hire another employee.

It can help you to know, in advance, if it is more profitable to

purchase cylinder heads from an existing vendor or to buy the equipment

necessary to rebuild them yourself. Keep in mind that if your company

is not growing or if your company is downsizing because of the local

economy – your fixed costs will not change!

At a minimum, you should calculate your break-even point on an

annual basis. But the facts are that your expenses vary throughout the

year. It would be appropriate to make one annual projection of your

break-even point, but then to monitor it on a monthly basis. It would

be good to know the break-even point any time you are considering a new

equipment purchase or hiring another employee.

There is certainly a great deal of financial information you need to

know about your company. The break-even point should be one of these

bits of financial information that you should monitor regularly. It is

well worth the effort!

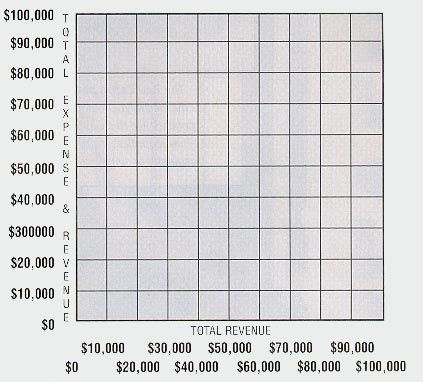

Below you’ll find a mathematical formula for calculating your

break-even point. The graph can be used to calculate the break-even,

too. Within this formula, we’ve provided expenses for a sample company.

We’ve used this information to demonstrate what the dollar amount of

fixed and variable expenses would be.

Keep in mind that there are differences of opinion as to whether

some expenses should be calculated as fixed or as variable costs. Some

may even argue for splitting out certain costs to more accurately

reflect your break-even point. Just remember your primary objective –

knowing what your break-even point is. When you know the dollar amount

that you must generate, no matter what the sales are, before you can

begin earning a profit, you’ll make better business decisions for your

company.

How To Establish Your Break-Even Point

Definition of Terms

BE-Sales at break-even point, FC-Fixed cost, VC-Variable cost, TR-Total revenue, TC-Total cost (Fixed cost + Variable cost)

Sample Values For Calculating Break-even Point

BE=FC($25,000) divided by (1 -VC($45,000) divided by TR ($90,000),

BE=FC ($25,000) divided by 0.5, BE=$50,000

- Draw a horizontal line at the point of fixed cost (FC). In the above example FC is $25,000.

- Draw a line from the left side of the fixed cost line, sloping

upward to the point where Total Cost (TC = Fixed cost + Variable cost)

meets $70,000 on the vertical column (Total Expense & Revenue), and

meets $90,000 on the horizontal base line (Total Revenue). This is a

line connecting point A to point C. - Draw a Total Revenue line from zero through to the point at

which $90,000 on the vertical column (Total Expense & Revenue)

meets $90,000 on the horizontal base line (Total Revenue). This is a

line connecting point D to point E. - The Break-even Point is the point where the Variable Cost

line (A-C) intersects the Total Revenue line (D-E). In this example it

is at $50,000.

Break-even

point analysis is a valuable financial decision-making tool. Break-even

analysis can help with making a decision relative to pricing your

products or services, or your equipment or tooling purchases. It can

also help with maintaining the appropriate level of employees, both

salaried and hourly.

Knowing your break-even point will enable you to establish daily,

weekly or monthly sales needed in order for your company to turn a

specific profit. Use the graph above to calculate your own break-even

based on the explanations found in our sample break-even analysis in

the top graph.