Most rebuilders will tell you that the market

has never been more competitive than it is today. Many will also

tell you that the past 12-18 months have been difficult in terms

of maintaining their sales levels of rebuilt units.

However, although total units sold may be down

industry wide, according to a recent survey of 1,000 jobbers across

the U.S., the percentage of rebuilt versus new parts sold in most

product categories is higher than it has ever been.

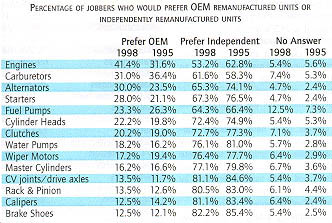

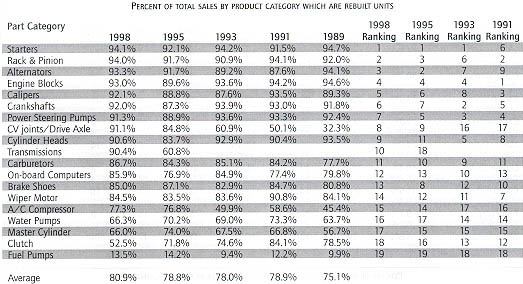

In fact, of 19 product lines sold by jobbers,

18 have higher rebuilt compared to new unit sales compared to

those sold in 1995. In 10 of those product lines jobbers report

that rebuilt units represent 90% or more of all units sold.

The product with the highest percentage of

rebuilt units sold is alternators at 94.1%. Rounding out the top

10 are rack-and-pinions (94%), alternators (93.3%), engine blocks

(93%), calipers (92.1%), crankshafts (92%), power steering pumps

(91.3%), CV axles (91.1%), cylinder heads (90.6%) and transmissions

(90.4%).

Although not representing 90% or more of total

product line sales, carburetors (86.7%), on-board computers (85.9%),

brake shoes (85%), wiper motors (84.5%), A/C compressors (77.3%),

water pumps (66.3%) and master cylinders (66%), all had significantly

higher sales of rebuilt versus new unit sales.

The only product lines with comparative or

fewer rebuilt units versus new units sold were clutches (52.5%

rebuilt) and fuel pumps (13.5% rebuilt). Fuel pumps have been

the product line with the highest percentage of new unit sales

since we began our survey study back in 1988.

Clutches, on the other hand, began a steady

downward progression of rebuilt unit sales beginning in the early

’90s when the influx of offshore new units available in the market

began to grow, as did the growing number of crimped cover clutch

design equipped vehicles. Since then an increasing number of rebuilders

have become distributors of new rather than manufacturers of rebuilt

units.

The reasons for increasing new unit sales of

clutches are a combination of their attractive price as well as

the difficulty that most rebuilders have when it comes to sourcing

parts for and rebuilding newer crimped cover clutch designs.

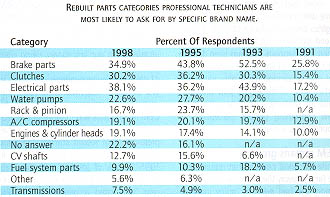

Of the 19 product lines surveyed, 14 actually

saw increases in rebuilt versus new unit sales. All product lines

with 90% or more of total sales represented by rebuilt units saw

increases in rebuilt versus new unit sales. One of those product

categories, transmissions, actually rose a staggering 29.6% in

rebuilt versus new unit sales.

In fact, several other product lines actually

saw significant increases in rebuilt versus new unit sales as

well. CV shafts, for example, rose from 84.8% rebuilt sales in

1995 to 91.1% rebuilt sales in 1998. Cylinder heads also rose

in rebuilt sales from 83.7% to 90.6% in 1998.

The increase in rebuilt unit sales within most

product categories points to the greater value that jobbers continue

to feel these products offer their retail and wholesale customers.

When asked to quantify their purchases of rebuilt parts jobbers

ranked warranty, quality, order fill, price and their previous

experience with the product, in that order, when considering the

purchase of a rebuilt product line.

About seventy-four percent of jobbers said

warranty was most important when making a rebuilt product line

purchasing decision. Warranty was followed by brand quality (69.2%),

order fill (63.4%), price (60.8%) and previous experience with

the product, which was cited by 47.1% of survey respondents.

Parts warranty actually showed the largest

percentage increase in importance from our last survey. A little

more than 69% of jobbers cited it as very important in 1995 compared

to 74.5% who ranked it as very important in this year’s survey.

The increase in the length of warranties is

viewed by many rebuilders as an extension of liability, especially

on products such as engines or cylinder heads that can fail within

the warranty period due to customer misuse or service neglect.

On the other hand, extended warranties are

viewed by many in our industry as a necessary marketing tool to

compete with OEM new and remanufactured products, as well as the

rising expectations by consumers for better performance and quality

of vehicle replacement parts.

Unfortunately, a longer warranty does not necessarily

indicate a better product. It’s no secret that many extended warranties

come with a plethora of "small print" which negates

coverage when either the installer or end user does not fulfill

specific criteria. When that happens, little has been done to

enhance the opinion of the installer or the end user concerning

the quality, value and performance of his rebuilt part purchase.

Quite the contrary, a lot of harm has been done concerning positive

perceptions of rebuilt products overall.

OEM remans growing

While the good news is that rebuilt parts are

far and away the preferred replacement option, the bad news for

many independent rebuilders is that OEM rebuilt parts have, in

many cases, seen an increase in jobber purchasing preferences.

Of 14 product lines researched, jobbers reported that they had

increased the percentage of OEM rebuilt versus independently rebuilt

parts in eight of those product lines.

OEM rebuilt engines saw the largest increase

from our last survey, being cited as the preferred replacement

option by 41.4% of survey respondents compared to just 31.6% of

respondents in 1995. The next largest increase in preference for

OEM rebuilt units was in rotating electrics. Twenty-eight percent

of jobbers said they preferred OEM rebuilt starters compared to

just 21% who said so in 1995. And in 1995 23.5% of jobbers said

they preferred OEM rebuilt alternators while this year 30% cited

a preference for OEM remanufactured units.

While the increase in purchasing preferences

was much smaller, usually anywhere from less than 1- 4 percentage

points, jobbers also reported a growing preference for OEM versus

independently rebuilt units in cylinder heads, clutches, water

pumps, CV shafts, rack-and-pinions and brake shoes.

Although the increase in OEM preference for

rebuilt units is marginal in some product categories, and despite

the fact that independently sourced parts still maintain the majority

of market share in all product lines that we surveyed, the overall

trend seems unmistakable.

The cost of warranty work in terms of time,

money and customer inconvenience is a growing issue for many service

technicians. Although usually a more expensive alternative, OEMs

have done a good job of promoting the performance and "original"

replacement part quality of their own remanufactured products.

Judging from the increase across the board in OEM rebuilt unit

sales, it appears more service technicians are listening.

Such trends point to the growing need for quality

rebuilt units. It also points to the need for the independent

aftermarket to continue to fight for access to on-board diagnostic

(OBD) information necessary to ensure that service problems are

diagnosed correctly, and that a replacement part can be rebuilt

and installed properly. Although access to such information is

currently mandated within existing Clean Air legislation, more

than a few OEMs have made it difficult, if not impossible, to

source.

Reinforcing the concern for quality of a rebuilt

replacement part, fewer jobbers said that the quality of rebuilt

parts which they use has increased. In fact, a higher percentage

of jobbers than ever reported that the quality of rebuilt parts

which they purchase has declined.

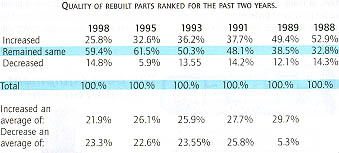

This year just 25.8% of jobbers reported that

the quality of rebuilt parts which they use has increased over

the past two years. In our 1995 survey, 32.6% of survey respondents

said quality had improved.

In this year’s survey, 14.8% of jobbers reported

that the quality of rebuilt parts, overall, has decreased over

the past two years compared to just 5.9% who said quality levels

had declined in our 1995 survey.

Similarly, for those reporting that quality

had increased, the average increase was less than all previous

years, and for those reporting that quality had decreased, the

average decrease was the highest since 1991.

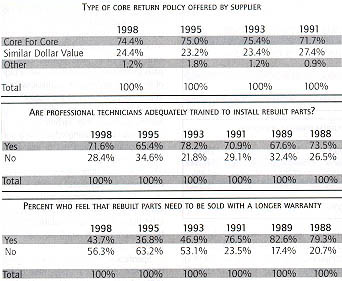

Survey data indicates that an overwhelming

percentage of jobbers would prefer to see rebuilt parts built

to an industry quality standard. When asked if they would like

to see such a standard developed for rebuilt units, a little more

than 84% of all jobbers responded yes. That compares to 85.4%

who said so in our 1995 survey.

Although the percentage of jobbers saying they

wanted to see a standard for quality developed declined by about

1 percentage point, the percentage of jobbers who said they would

be willing to pay a higher price for units built to such standards

rose significantly. Nearly 80% of survey respondents reported

they would be willing to pay more for a part built to a uniform

quality standard compared to just 72.6% who said they would in

our 1995 survey. The increases in purchasing preferences for many

OEM rebuilt units discussed earlier seems to provide evidence

of such intent.

The price issue

In addition to questions concerning quality,

we also asked jobbers to tell us which rebuilt products their

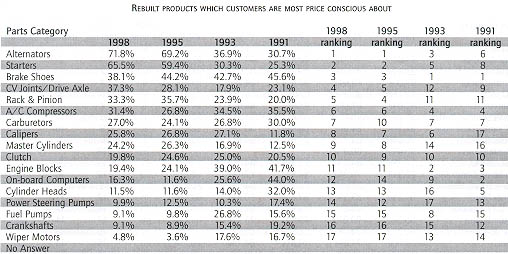

customers were most price conscious about. The ranking of the

top three rebuilt units in terms of price concerns was the same

as in our 1995 survey.

Alternators, starters and brake shoes were

ranked one, two and three in terms of customer concerns over price.

However, the percentage of jobbers who said price was a top concern

increased for alternators and starters, while the number of jobbers

reporting that price was an issue for brake shoe purchases declined.

Specifically, nearly 72% of jobbers ranked

alternators as one of their top five "price conscious"

products compared to 65.5% who said the same for starters. In

our 1995 survey a little more than 69% of jobbers said alternators

were ranked in the top five price concern products while 59.4%

said the same for starters. A little more than 44% of jobbers

said that brake shoes ranked in the top five price concern products

in 1995 compared to just 38% who said so in this year’s survey.

Despite the fact that warranty coverage ranks

as the most important factor when making a rebuilt parts line

purchase decision, price is still a major concern. Rebuilt alternators,

starters, CV shafts, A/C compressors, carburetors, on-board computers,

crankshafts and wiper motors were all rated as more price sensitive

products compared to their 1995 rankings. On the other hand, brake

shoes, rack-and-pinion, calipers, master cylinders, clutches,

engine blocks, power steering pumps and fuel pumps were ranked

as less price sensitive. Of all rebuilt parts sold, wiper motors,

crankshafts and fuel pumps were ranked as the least price sensitive

compared to other rebuilt products.

In general, when trying to understand the impact

of price and warranty when it comes to jobber purchasing decisions,

it is obvious that both the professional service installer and

the consumer have come to expect more.

What sells the most

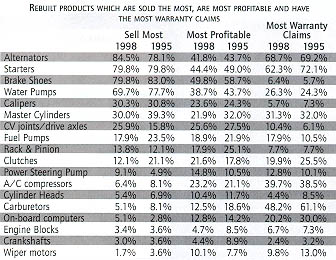

Topping the list of highest number of units

sold is alternators. A little more than 84% of jobbers said that

alternators were among the top five rebuilt parts sold. Alternators

were followed by starters (79.8%), brake shoes (79.8%), water

pumps (69.7%), calipers (30.3%), master cylinders (30.0%), CV

shafts (25.9%), fuel pumps (17.9%), rack-and-pinions (13.8%) and

clutches (12.1%). All other products each accounted for less than

10% of jobbers ranking them among their top five parts sold.

Although the top 10 volume producers were the

same products listed in our 1995 survey, their rankings changed

somewhat. Among the top three sales leaders, for example, alternators

replaced brake shoes as the number one volume product this year.

In our 1995 survey alternators ranked number three in volume.

Starters retained the number two position in units sold.

Readers should keep in mind that sales volume

rankings are industry averages. There, of course, are jobbers

who might specialize in certain product lines depending on geographic

location and customer base.

Highest profit products

Although alternators displaced brake shoes

as the leading rebuilt part sold in terms of volume, brake shoes

retained their ranking as the most profitable rebuilt product

line. Nearly 50% of all jobbers ranked brake shoes among the top

five most profitable products they sell. Brake shoes were followed

by starters (44.4%), alternators (41.8%), water pumps (38.7%),

CV shafts (25.6%), calipers (23.6%), A/C compressors (23.2%),

master cylinders (21.9%), clutches (21.6%) and fuel pumps (18.9%).

As with our explanation of sales volume, readers

should keep in mind that profit rankings are industry wide generated

averages. Often times statistics can be just as revealing about

what they don’t say as what they do say. We suspect that some

product rankings in terms of profits are based on "total"

profit dollars generated rather than profit "margins"

of specific product lines.

Jobbers, for example, that may not sell many

crankshafts or engine blocks may not be reporting these products

as higher profit generating products compared to alternators and

starters which they sell in significant numbers.

Highest warranty products

We also asked jobbers to tell us which products

were among their highest warranty returns. Alternators were number

one on jobbers’ headache list, claimed by nearly 69% of jobbers

to be among the top five products returned as a warranty claim.

Alternators were followed by starters (62.3%),

carburetors (48.2%), A/C compressors (39.7%), master cylinders

(31.3%), water pumps (26.3%), on-board computers (20.2%), clutches

(19.9%), fuel pumps (17.9%) and power steering pumps (12.8%).

Although the percentage of jobbers ranking

alternators and starters within the top two warranty return categories

was lower, these two products repeated in the top two categories

again this year. Jobbers said both professional installers and

do-it-yourselfers continue to make unintended misdiagnosis of

vehicle electrical system problems. So, too, do they sometimes

install rebuilt units as diagnostic tools to help locate the actual

no-start or charging problem on the vehicle.

Computer controlled vehicles increasingly present

both retail and wholesale purchasers of rebuilt units with diagnostic

and correct installation problems. Warranty return rankings of

these two units, especially, point to the continued need for the

rebuilding industry to fight for access to on-board diagnostic

tools and information from the OEMs in order to make properly

rebuilt units available. They also point to the importance of

rebuilders having the proper testing equipment to ensure that

rebuilt units operate as they should.

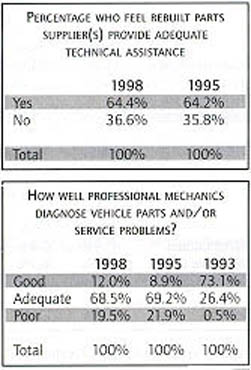

As our survey results indicate, the expectations

for higher quality rebuilt parts are rising. But so are those

for proper diagnosis and installation. Survey results indicate

that jobbers are more pleased with the diagnostic and installation

skills of professional installers.

When asked if professional technicians are

adequately trained to install rebuilt parts, 71.6% of jobbers

responded yes. It is the highest percentage ever reported, and

an increase of a little more than 6 percentage points compared

to the 65.4% of jobbers who said technicians were adequately trained

in our 1995 survey.

Although the percentage point increases were

marginal in most product lines, all parts showed an increase in

the percentage of time that professional technicians were able

to correctly diagnose the original vehicle part or system problem.

This year 12% of jobbers reported that technicians did a "good"

job of diagnosing vehicle parts and service problems compared

to just 8.9% who said so in 1995.

A little more than 68% said that technicians

did an "adequate" job (69.2% said so in 1995) of diagnosing

parts and service problems, while 19.5% said technicians did a

"poor" job on vehicle diagnostic work compared to nearly

22% who said so in our 1995 survey.

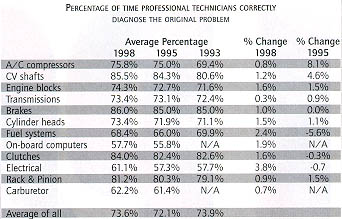

Specifically, the parts with the highest diagnostic

satisfaction ratings were brakes (86% of jobbers said problems

with them were correctly diagnosed), followed by CV shafts (85.5%),

clutches (84%), rack-and-pinions (81.2%), A/C compressors (75.8%),

engine blocks (74.3%), cylinder heads (73.4%), transmissions (73.4%),

fuel systems (68.4%) and carburetors (62.2%). Electrical (61.1%)

and on-board computers (57.7%) received the lowest satisfaction

ratings when it came to proper diagnostic work by professional

technicians. There has been an increase in the satisfaction with

technician diagnostic and installation work. But when just 12%

of jobbers say that technicians do a "good" job at it,

there remains a lot of improvement work yet to be realized.

Lastly, we asked jobbers for their perspectives

on sourcing, core policy, length of time doing business with the

same supplier, preference for product packaging, training and

sales/promotion support.

With the industry-wide number of consolidations

taking place among both suppliers and rebuilders you would think

that more jobbers would be purchasing their parts from a single

supplier. However, more jobbers said they preferred sourcing their

parts from multiple sources. This year 41.8% of jobbers reported

a preference for using multiple suppliers compared to 39.8% who

said so in 1995.

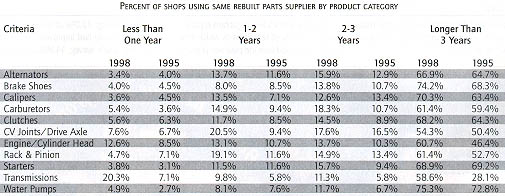

The length of time that jobbers have stayed

with a source of rebuilt product has increased virtually across

all product lines. We asked jobbers to indicate the number of

years they had used the same supplier in 11 different product

categories. In the three years or longer category, the percentage

of jobbers responding was higher in every product line except

for starters where it declined less than 1 percentage point.

Transmissions and engines/cylinder heads showed

the largest increase in the number of jobbers that have used the

same source for three years or more. Interestingly, the largest

percentage of jobbers indicating they had used a supplier for

less than one year was also in the transmissions and engines/cylinder

head categories. This seems to indicate there are many jobbers

who are unhappy with their current source in these product lines,

however, once they find a source for those products they like,

they are reluctant to change. The higher cost in inventory, warranty

and customer satisfaction are the likely explanation.

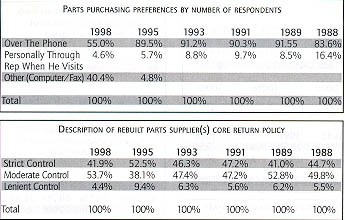

Not much has changed in terms of core return

policies. Nearly three-quarters of all jobbers report that their

suppliers require a core-for-core return policy compared to 75%

who said so in 1995. Those receiving a "similar dollar value"

core policy rose from 23.2% in 1995 to 24.4% this year.

Although fewer jobbers reported that their

core return policies were "strictly" controlled ( 41.9%

this year versus 52.5% in 1995), a significantly higher number

(53.7%) said their core return policies were "moderately"

enforced compared to just 38.1% who said so in 1995.

Part number proliferation and the desire to

reduce inventory and warranty expenses, wherever possible, are

the primary reasons for more stringent control of core returns.

In most product lines, profit margins are being squeezed and rebuilders

are being forced to implement more efficient core return policies.

As to rebuilder efforts to promote and advertise

rebuilt products, jobbers ranked the personal sales call as the

most effective sales tool. The personal sales call was also number

one in 1995, although the percentage of jobbers saying it was

most effective rose from 31.6% in 1995 to 35.6% this year.

The personal sales call was followed by seminars/technical

clinics (31.3%), trade magazine advertising (10.7%), direct mail

(7.7%) and telemarketing (0.4%) as the most effective sales and

promotional tools of rebuilders.

Once a decision was made to buy, however, preferences

for the best procedure for placing an order have changed dramatically.

In 1995, 89.5% of jobbers said that the telephone was the preferred

way to order parts. This year, just 55% of jobbers said so.

The telephone still ranks as the most popular

method for placing an order. However, where just 4.8% of jobbers

said the computer/fax was the best approach to order placement

in 1995, a whopping 40.4% of jobbers said it was the preferred

method for placing an order this year.

In sum, there seems to be no question that

technology continues to significantly impact vehicle diagnostics

and parts installation, as well as the way in which rebuilt parts

are purchased, processed and rebuilt.